최대 3천만원까지 외국인 체류자격별로 생활자금 등을 지원하는 외국인 전용 대출상품 JB Bravo KOREA대출(전북은행) 입니다. 본 글에서는 국내 거주하는 외국인 고객님들을 위한 대출 상품에 관한 중요한 정보를 제공해 드리려 합니다.

JB Bravo KOREA Loan (Jeonbuk Bank) is a loan product exclusively for foreigners that supports living expenses up to 30 million won, depending on your status of residence. In this article, we will provide important information on loan products for foreigners living in Korea.

전북은행에서 취급하고 있는 JB Bravo KOREA대출상품은 대한민국에서 생활하시는 외국인분들도 금융 서비스를 필요로 하시며, 때로는 예기치 못한 경제적 어려움을 겪으실 수 있는 상황에서 안정적인 금융 지원을 받으시어 여러분의 경제 활동이 보다 원활하게 이루어질 수 있도록 돕고자 설계되었습니다.

The JB Bravo KOREA loan product, offered by Jeonbuk Bank, is designed to help foreigners living in Korea to receive stable financial support in situations where they may need financial services and sometimes face unexpected financial difficulties, so that their economic activities can run more smoothly.

💡관련 : 대출받는 순서는 알고 계시나요? 1금융 2금융(저축은행, 캐피탈) 3금융(대부업) 까지 정리

더불어 대안으로 고려될 수 있는 다른 대출 상품에 대한 정보도 함께 제공하겠습니다.

구독하고 계신 분들에게 도움이 되는 정보가 되었으면 좋겠습니다.

✅참고하면 좋은 글 : 정부지원 대출 4대장

- 정부지원 새희망홀씨2 대출자격과 대출금리 알아보기

- 정부지원 햇살론 대출자격과 대출금리 알아보기

- 정부지원 사잇돌대출과 사잇돌2대출 비교와 대출조건 알아보기

- 정부지원 새희망홀씨 대출 알아보기

전북은행 JB Bravo KOREA 개요(Overview of Jeonbuk Bank JB Bravo KOREA)

| 구분 | 내용 |

| Loan to | 대출 신청일 현재 체류자격 E-9(비전문취업), F-5(영주), F-6(결혼이민), E-7(특정활동), F-2(거주)로 국내에 거주중 Residing in Korea with a status of residence of E-9 (non-professional employment), F-5 (permanent resident), F-6 (marriage immigrant), E-7 (specific activity), or F-2 (residence) on the date of loan application. |

| Loan limits | 동일인당 최소 1백만원 이상 ~ 최대 30백만원 이내 (10만원 단위) Minimum of 1 million won and maximum of 30 million won per person (in increments of 100,000 won) |

| Loan rate | 최저 연 10.39% ~ 최고 연 15.00% (신용등급별 차등 적용) Lowest 10.39% APR to highest 15.00% APR (sliding scale based on creditworthiness) |

| Loan Term | 3개월 이상 36개월 이내(월단위) More than 3 months but less than 36 months (in months) |

위의 정리된 표와 같이 전체개요입니다. 자세한 내용은 아래에 더 설명하겠습니다.

전북은행 JB Bravo KOREA 대상(Jeonbuk Bank JB Bravo KOREA Qualification)

전북은행의 외국인 대출 외국인(체류자격별)을 대상으로 생활자금 등을 지원하는 외국인 전용대출 상품입니다.

Jeonbuk Bank’s Foreigner Loan is a loan product exclusively for foreigners (by status of residence) to support living expenses.

기본적으로 아래 체류자격별 비자에 따라 자격기준이 다르니 참고하시기 바랍니다.

Basically, there are different eligibility criteria for each of the visas below.

【체류자격별 자격기준】

소득증빙이 가능한 19세 이상만 가능하며 NICE 신용평점 590점 이상이어야 합니다.

💡관련 : 정부지원 무직자 대출이 있다는 사실 알고 계신가요?

대상

- 대출 신청일 현재 체류자격 E-9(비전문취업), F-5(영주), F-6(결혼이민), E-7(특정활동), F-2(거주)로 국내에 거주중이며 체류기간 만료일자(근로계약기간)가 3개월 이상 남은 자로(F-5제외), 다음의 체류자격별 자격기준을 충족

- 외국인소득증빙이 가능한 만 19세 이상 & NICE 신용평점 590점 이상 고객 중

- As of the date of loan application, you are living in Korea with a status of residence of E-9 (non-professional employment), F-5 (permanent residence), F-6 (marriage immigration), E-7 (specific activity), or F-2 (residence), and your expiration date (work contract period) is more than 3 months away (except for F-5), and you meet the following eligibility criteria for each status of residence.

- 19 years of age or older with proof of foreign income & NICE credit score of 590 points or more

전북은행 JB Bravo KOREA 조건(Conditions for Jeonbuk Bank JB Bravo KOREA)

신청은 영업점에서만 가능합니다! 모바일 또는 온라인으로는 자격이 되지 않으니 유의하시기 바랍니다!

Please note that you can only apply in-store – mobile or online does not qualify!

💡관련 : 마통(마이너스통장) 개념 및 사용법과 이자계산법

대출한도는 소 1백만원 이상 ~ 최대 3천만원 이내이며 10만원 단위로 가능합니다!

The loan limit is between 1 million won and up to 30 million won, in increments of 100,000 won!

대출기간 3개월 이상 36개월 이내이며 월단위로 설정가능합니다!

Loan term of at least 3 months but not more than 36 months and can be set on a monthly basis!

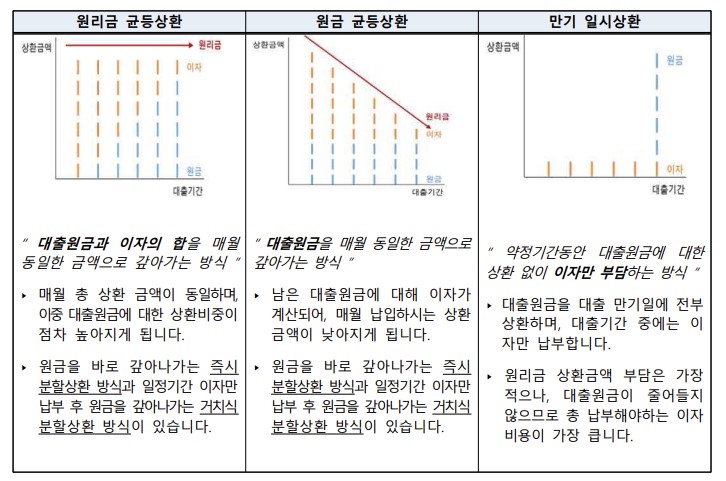

상환방법은 원금균등분할상환(원금은 약정된 분할상환납입일(매월 등)에 균등 분할상환하고, 이자는 원금 상환방법과 동일한 월단위 또는 1개월 단위로 후취) 또는 원리금균등분할상환(원금과 이자를 합하여 약정된 분할상환납입일(매월 등)에 같은 금액으로 후취)입니다.

The repayment method is either equal installments (the principal is repaid in equal installments on the scheduled payment date (monthly, etc.), and the interest is collected in the same monthly or one-month increments as the principal repayment method) or equal installments (the principal and interest are combined and collected in the same amount on the scheduled payment date (monthly, etc.)).

더 자세한 내용은 아래 그림을 보고 참고하시기 바랍니다!

조건

- 대출한도 : 동일인당 최소 1백만원 이상 ~ 최대 30백만원 이내 (10만원 단위)

- 대출기간 : 3개월 이상 36개월 이내(월단위)

- 대출금리 : 최저 연 10.39% ~ 최고 연 15.00% (신용등급별 차등 적용)

- 상환방법 : 원금균등분할상환, 원리금균등분할상환

- Loan limit: Minimum 1 million won to maximum 30 million won per person (in increments of 100,000 won)

- Loan term: 3 months to 36 months (monthly)

- Interest rate: Minimum 10.39% ~ Maximum 15.00% per annum (differentiated by credit rating)

- Repayment method: Equal installments, equal repayment of principal

✅상환방법별 특징 참고

전북은행 JB Bravo KOREA 기타사항(Jeonbuk Bank JB Bravo KOREA Others)

계약 체결 전 상품설명서 및 약관을 확인하시기 바랍니다.

Please read the product description and terms before entering into a contract.

해당 상품에 대해 충분한 사전 설명을 받을 권리가 있으며, 설명을 이해한 후 거래하시기 바랍니다.

You are entitled to a full explanation of the product before you trade, and please make sure you understand the explanation before you trade.

대출 금리는 약정기간까지 고정금리입니다.

The interest rate on your loan is fixed until the end of the term.

대출금리 산출기준

- 최저 : 내부신용등급 JBCR 1등급, 대출금액 10백만원, 대출기간 12개월, 고정금리

- 최고 : 내부신용등급 JBCR 9등급, 대출금액 10백만원, 대출기간 12개월, 고정금리

- 기준금리 : 연 3.92% (시장기준금리 금융채AA+)

- 가산금리 : 신용등급에 따라 최저 연 6.47% ~ 최고 연 11.08%

- 약정기간까지 고정금리 (금리변동주기 없음)

- Lowest : Internal credit rating JBCR 1, loan amount 10 million won, loan term 12 months, fixed interest rate

- Highest: Internal credit rating JBCR 9, loan amount of KRW 10 million, loan period of 12 months, fixed interest rate

- Base rate: 3.92% p.a. (market rate financial bond AA+)

- Additional interest rate: Minimum 6.47% ~ Maximum 11.08% per annum depending on credit rating

- Fixed interest rate until the contract period (no interest rate change cycle)

중도상환수수료

- 상환 잔존기간이 3개월 초과시 중도상환수수료 부과

- 중도상환수수료율 : 잔존기간 1년 이하 연 1.0% / 잔존기간 1년 초과 연 2.0%

- 수수료 산정방법 : 중도상환금액 × 중도상환수수료율 × 대출잔여일수 / 대출기간

- Early redemption fee charged if the remaining repayment period exceeds 3 months

- Early repayment fee rate: 1.0% per year for 1 year or less / 2.0% per year for more than 1 year

- Fee calculation method: Mid-term repayment amount × mid-term repayment fee rate × loan remaining days / loan period

구비서류

- 자격확인서류 : 외국인등록증, 표준근로계약서, 외국인 고용허가서 등

- 재직확인서류 : 재직증명서, 건강보험 자격득실 확인서 등

- 소득확인서류 : 근로소득원천징수영수증, 소득금액증명원, 급여명세표 등

- (※체류자격 / 고용형태에 따라 준비서류가 일부 다를 수 있음)

- Eligibility verification documents: Alien registration card, standard labor contract, foreign employment permit, etc.

- Employment verification documents: employment certificate, health insurance eligibility certificate, etc.

- Income verification documents: Income tax receipt, source of income, paycheck stub, etc.

- (*Documents may vary depending on your status of residence/employment type)

취급제한

- 「신용정보관리규약」상 연체정보, 대위변제대지급정보 등 연체등록자

- 개인회생절차가 개시된자, 신용회복지원이 확정된자, 파산신청자 또는 파산 선고자

- 당행 연체대출금 또는 대지급금을 보유하고 있는자

- (※ 그 외 신용등급 및 당행의 심사기준에 따라 대출이 거절 될 수 있음)

- “Persons registered as delinquent under the Credit Information Management Regulations, including delinquency information and subrogation payment information.

- Individuals who have initiated personal rehabilitation proceedings, those who have received credit recovery support, bankruptcy applicants, or those who have been declared bankrupt.

- Persons who have overdue loans or payments to the Bank

- (* Loans may be denied based on other credit ratings and the Bank’s screening criteria)

💡관련 : 외국인 대출가능한 곳 Top5 정리

대출 이자계산 방법(How interest is calculated on loans)

일반적인 이자 계산 방식(Common interest calculation methods)

대출금에 연이율을 곱한 값에 대출 기간(일수)를 다시 곱하고, 그 결과를 1년(365일, 윤년인 경우 366일)로 나눠서 이자를 산출합니다. 여기서 원 단위 미만은 절사합니다.

The interest is calculated by multiplying the loan amount by the APR, multiplying it again by the loan term in days, and dividing the result by a year (365 days, or 366 days if it’s a leap year). Here, anything less than a circle is truncated.

원리금 균등분할상환 대출(Equalized Principal Amortization Loans)

월별로 지불해야 할 이자는 대출 원금에 연이율을 곱한 후, 그 결과를 12로 나누어 산출합니다.

The interest due each month is calculated by multiplying the loan principal by the APR and dividing the result by 12.

일수 계산(Counting days)

일반적으로 대출을 받은 당일로부터 상환일 전일까지의 기간을 기준으로 합니다.

It’s typically based on the period from the day you take out the loan until the day before the repayment date.

하지만 특정 상황에서는 대출 당일부터 상환일까지를 기준으로 합니다.

However, under certain circumstances, it is based on the date of the loan to the date of repayment.

이러한 상황은 대출금이 대출 당일에 회수되는 경우, 대외 기관으로부터 자금을 차입하여 이자를 상환일까지 지급하는 경우, 연체기간이 1일인 경우, 그리고 대여 유가증권에 해당됩니다.

This is true when the loan is collected on the same day as the loan, when funds are borrowed from an external entity and interest is paid until the repayment date, when the overdue period is one day, and for lending securities.

원금 균등분할상환대출(Equal Principal Amortization Loans)

이자는 대출금액과 대출이자율을 곱한 값에 이자 일수를 다시 곱하고, 그 결과를 1년(365일, 윤년은 366일)로 나누어 산출합니다.

Interest is calculated by multiplying the loan amount and the loan interest rate by the number of interest days again, and dividing the result by a year (365 days, 366 days in leap years).

원리금 균등분할상환대출(Equal Principal Amortization Loan)

이자는 대출금액과 대출이자율을 곱한 후 그 결과를 12로 나누어 산출합니다.

Interest is calculated by multiplying the loan amount by the loan interest rate and dividing the result by 12.

💡관련 : 연체 걱정되시나요? 정부 채무조정 지원 안내

대출 FAQ

한도조회를 해도 정말 내 개인신용평점에 영향이 없나요?(Does inquiring about limits really affect my credit score?)

네, 없습니다. 대출한도 조회 및 대출 신청만으로는 신용도(개인신용평점 등)에 영향을 미치지 않으며, 대출이 실행되면 신용조회기록이 남게 됩니다.

No, inquiring and applying for a loan does not affect your creditworthiness (such as your personal credit score), and once the loan is executed, you will have a credit history.

대출계약의 체결만으로도 개인신용평점이 하락할 수 있으며, 대출계약이 변제 혹은 이에 준하는 방식으로 거래가 종료된 경우에도 일정기간 개인신용평점의 산정에 영향을 줄 수 있습니다.

The signing of a loan agreement alone can lower your credit score, and even if the loan agreement is repaid or otherwise terminated, it may affect the calculation of your credit score for a period of time.

대출 받은 후 철회가 가능할까요?(Can I withdraw after taking out a loan?)

네, 가능합니다. 대출 계약 후 14일 이내 청약철회가 가능하며,증액대출 및 일부 중도상환 시에는 철회가 불가합니다.

Yes, you can. You can cancel within 14 days of signing the loan agreement, except for incremental loans and some early repayments.

청약철회권을 행사한 경우에는 중도상환수수료가 면제되며,5영업일 이내에 해당 대출과 관련한 대출정보가 삭제됩니다.

If you exercise your right of rescission, we’ll waive the prepayment penalty and remove the loan information associated with the loan within 5 business days.

또한, 청약철회권의 효력이 발상한 이후에는 이를 취소할 수 없습니다.

In addition, once a right of withdrawal has been triggered, it cannot be revoked.

💡관련 : 대출 철회하고 싶다구요? 대출 철회 시 주의사항

대출금을 연체할 거 같은데 불이익은?(I’m going to default on my loan, what’s the penalty?)

대출 원리금을 5영업일 이상 연체한 경우 단기연체정보가 신용정보회사에 제공되어 금융거래 제한(신용카드 정지 등)받을 수 있고, 개인신용 점수 하락 및 이에 따른 금리상승 등 불이익이 발생할 수 있으며 단기연체정보 등록 후 대출 원리금을 변제하여 단기연체정보가 해제되어도 개인신용점수가 일정기간 회복되지 않을 수 있습니다.

If you are more than 5 business days behind on your loan payments, short-term delinquency information will be provided to the credit bureau, which may result in financial transaction restrictions (such as credit card suspension), a decrease in your personal credit score and a corresponding increase in interest rates, and your personal credit score may not recover for a period of time even if the short-term delinquency information is removed by repaying the loan principal after registration.

대출 원리금을 3개월 이상 연체한 경우 그 3개월이 되는 날을 등록사유발생일로 하여, 그 때로부터 7영업일 이내에 「일반신용정보관리규약」에 따른 연체정보가 등록됩니다.

If the loan principal is overdue for more than three months, the third month will be considered as the date of occurrence of the reason for registration, and delinquency information under the General Credit Information Management Regulations will be registered within seven business days from that date.

전북은행 JB Bravo KOREA 신청방법(How to apply for Jeonbuk Bank JB Bravo KOREA)

영업점에서만 대출이 가능하므로 유의하시기 바라며, 아래 안내하는 모바일 앱 또는 온라인 홈페이지는 참고사항으로 안내목적으로만 이용하시기 바랍니다!

Please note that loans are only available at branches, so please use the mobile app or online homepage below as a guide only!

대출상담 📞1588-4477으로 연락하시면 좀 더 세밀하게 상담 가능합니다.

Call us at 📞1588-4477 to discuss your loan in more detail.

📲어플 다운로드 및 설치

걱정마세요😘 대안상품(Don’t worry😘 Alternatives)

대출 신청이 거절된 이유는 다양하겠지만, 주로 신용도 또는 소득 문제로 거절되는 경우가 많습니다. 이런 상황에서는 정부의 신용회복 지원 대출이나 소액대출 등 다양한 프로그램을 이용해 보실 수 있습니다.

There are a variety of reasons why your loan application may have been denied, but often it’s due to credit or income issues. In this situation, you may be eligible for a variety of programs, including government credit repair loans or microloans.

💡관련 : 대부업 대출 받을 때 유의할 점

이 외에도 사회복지 시설을 통한 지원, 소비자금융 등에서 제공하는 대출상품도 참고하실 수 있습니다.

In addition, you may also be able to find assistance through social services, consumer finance, and other loan products.

대안상품

- 광주은행 햇살론15 총정리(신청대상 대상조건 신청방법 등)

- 햇살론 승인률 높은 금융사 안내합니다 고려저축은행

- 햇살론뱅크 대출도와드립니다(1금융 신한은행)

- 삼성생명 햇살론 조건확인 및 신청하기

- 하나은행 햇살론뱅크 조건확인 및 신청하기

대출 부결 사유 정리(Clean up loan denials)

대출심사 부결사유는 다양하고 각자의 상황에 따라 다릅니다. 특히 정부가 지원하는 대출상품들은 비교적 대출 승인이 잘 되는 경향이 있습니다만, 부결이 될 수 있는 상황이 있습니다.

There are a variety of reasons for loan rejections, and it all depends on your situation. While government-backed loans tend to be approved more often than not, there are circumstances that can lead to a rejection.

부결 사유는 심사에 따라 조금씩 다르겠지만 대표적인 공통점들은 다음과 같습니다.

Reasons for rejection will vary by review, but some common ones include

- 소득대비 기대출이 많은 경우

- 연체이력이 있는 경우

- 회생, 파산, 면책 등의 신청사실이 있는 경우나 금융사기 관련 기록이 있는 경우

- You have high expenses relative to your income

- You have a history of late payments

- Have filed for rehabilitation, bankruptcy, or discharge, or have a history of financial fraud.

✅<참고하기> 정부지원 대출 추천상품

정식 등록된 대부업체인지 확인(바로가기)

- 금융감독원 등록대부업체 통합조회 홈페이지 접속

- ‘대부업체검색’ 항목 란에 업체의 대부업체 명, 등록증번호, 대표자, 유효기간, 전화번호 등 조회 내용 확인

유효한 법정 최고금리 확인(바로가기)

정식 등록된 대부업체는 법적으로 연 20%를 초과하여 이자를 받을 수 없습니다. 이에 반하면 무조건 불법입니다.

✅그 외 참고하면 좋은 글

- 무직자 대출 쉬운 곳 5개 알아보기(정식등록업체기준)

- 무직자 대출 실제 받고 추천하는 곳 알아보기(가장 선호도 높고 많이 이용)

- 여성, 주부를 위한 안심대출 알아보기(여성전용)

- 대학생들이 이용하기 좋은 안심되고 신용도 높은 대출상품 알아보기

- 대부업 간편한 모바일 대출가능한 곳 알아보기(정식등록업체기준)

신용대출은 계획적으로 사용(필독)

자신의 금융상태 확인하기

신용대출을 받기 전 자신의 신용등급과 월별 수입과 지출 등을 정확하게 파악합니다.

대출 목적 명확화

대출을 받을 목적을 확실히 정하고나서 대출상품을 찾아야 합니다.

대출 상품 비교하기

여러은행과 금융 기관의 대출 상품을 비교하여 금리를 비교하고 대출조건이 좋은 상품을 선택합니다.

대출한도와 상환기간 결정

대출금액과 상환기간을 결정할땐 자신의 수입과 지출을 모두 고려하여 결정해야 합니다.

부수적 비용 고려

대출에 따라 발생하는 여러가지 부수적 비용(중도상환수수료 등)을 염두에 두고 대출을 실행하셔야 합니다.

정기적 대출 및 부채 관리

상환기간에 따른 정기적 대출상황 파악 및 대출실행 후에도 신용카드 부채 등 신용등급 하락을 관리해야 합니다.

💡관련 : 카드론 신용등급 하락의 진실과 회복기간